On-Premise Data Center Capacity Being Increasingly Dwarfed by Hyperscalers and Colocation Companies

RENO, NV, July 12, 2023

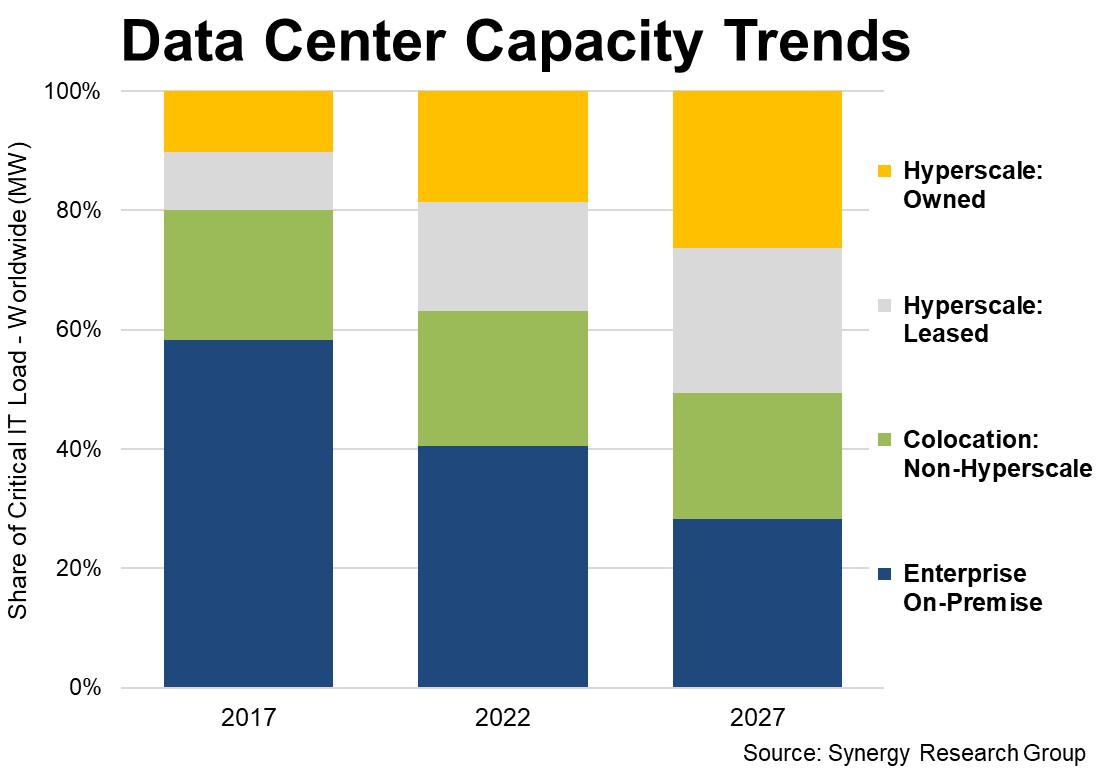

As the number of large data centers operated by hyperscale providers approaches 900, new data from Synergy Research Group shows that they now account for 37% of the worldwide capacity of all data centers. Approximately half of that hyperscale capacity is in own-built, owned data centers and half is in leased facilities. With non-hyperscale colocation capacity accounting for another 23% of capacity, that leaves on-premise data centers with just 40% of the total. This is in stark contrast to five years ago, when almost 60% of data center capacity was in on-premise facilities. Looking ahead five years, hyperscale operators will account for over half of all capacity, while on-premise will drop to under 30%. Meanwhile the total capacity of all data centers will continue to rise steadily, driven primarily by hyperscale capacity almost doubling over the next five years. While on-premise share of the total will drop by over two percentage points per year, the actual capacity of on-premise data centers will decrease only marginally. Colocation share of total capacity will remain relatively constant. The hyperscale research is based on an analysis of the data center footprint and operations of 19 of the world’s major cloud and internet service firms, including the largest operators in SaaS, IaaS, PaaS, search, social networking, e-commerce and gaming. The colocation and leased data center research is based on Synergy’s in-depth tracking of the colocation market, including quarterly data on over 230 individual companies.

The hyperscale research is based on an analysis of the data center footprint and operations of 19 of the world’s major cloud and internet service firms, including the largest operators in SaaS, IaaS, PaaS, search, social networking, e-commerce and gaming. The colocation and leased data center research is based on Synergy’s in-depth tracking of the colocation market, including quarterly data on over 230 individual companies.

Ten years ago, enterprises were spending over $80 billion per year on IT hardware and software for their own data centers, while spending well under $10 billion on nascent cloud infrastructure services. Fast forward to the present day and spending on data center hardware and software has only grown by an average 2% per year, while spending on cloud services has ballooned, growing by an average 42% per year to reach $227 billion in 2022. As enterprises radically reshaped their IT investments and crimped spending on their own data centers, the leading cloud providers rapidly built out huge global networks of hyperscale data centers. Hyperscale operator growth was further fueled by rapid development of more consumer-oriented digital services such as social networking, e-commerce and online gaming. Furthermore, while enterprises did maintain or slowly grow spending on data center equipment, a growing proportion of that gear has been pushed offsite into colocation facilities. On-premise data centers will not disappear any time soon, but their scale is being increasingly dwarfed by hyperscale and colocation companies.

About Synergy Research Group

Synergy Research Group, now part of TechInsights, delivers quarterly analyses of global IT and Cloud markets, offering detailed breakouts of vendor revenues and shipments by segment and region. Market shares and forecasts are provided through Synergy Interactive Analysis (SIA™) — the industry's only fully proprietary SaaS platform purpose-built for market share and forecasting analytics.

For more than 25 years, Synergy has been a trusted source of quantitative research and market intelligence across emerging communications and technology sectors. By combining syndicated research with specialized consulting, we deliver actionable intelligence to marketing and strategy executives worldwide.

A trusted source of accurate market data, Synergy is cited by industry leaders as well as leading financial, business, and trade publications such as The Economist, The New York Times, The Wall Street Journal, United States Federal Reserve Board, NPR, Forbes, Bloomberg, Financial Times, Bank of England, Fortune, and The Guardian.

About TechInsights

Regarded as the most trusted source of actionable, in-depth intelligence related to semiconductor innovation and surrounding markets, TechInsights’ content informs decision makers and professionals whose success depends on accurate knowledge of the semiconductor industry—past, present, or future.

Over 650 companies and 100,000 users access the TechInsights Platform, the world’s largest vertically integrated collection of unmatched reverse engineering, teardown, and market analysis in the semiconductor industry. This collection includes detailed circuit analysis, imagery, semiconductor process flows, device teardowns, illustrations, costing and pricing information, forecasts, market analysis, and expert commentary. TechInsights’ customers include the most successful technology companies who rely on TechInsights’ analysis to make informed business, design, and product decisions faster and with greater confidence. For more information, visit www.techinsights.com.

Subscriptions: sales@srgresearch.com

Press inquiries: heather.gallo@techinsights.com