Hyperscale Operators now Account for a Third of all Spending on Data Center Hardware & Software

RENO, NV, December 13, 2019

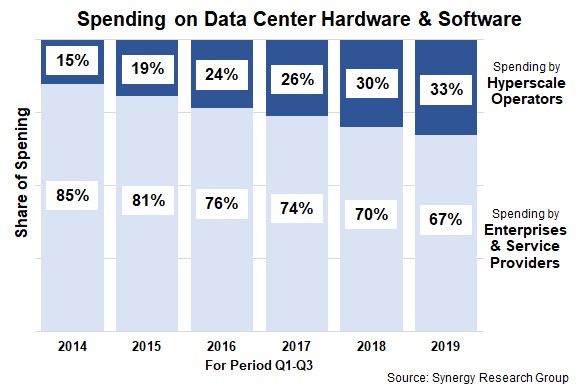

New data from Synergy Research Group shows that hyperscale operators accounted for 33% of all spending on data center hardware and software in the first three quarters of 2019, up from 26% in Q1-Q3 of 2017 and 15% in 2014. Over that same period the total market has increased in size by over 34%, with the vast majority of the growth being the result of increased spending by the hyperscale operators. Spending by enterprises and service providers has risen by just 6%. Increased spending by hyperscale operators has been driven by burgeoning demand for public cloud services and continued strong growth in social networking. Meanwhile enterprise spending has remained under pressure primarily due to the ongoing shift in workloads from private networks to the public cloud. Hyperscale operators include the world’s largest providers in the field of IaaS, PaaS, SaaS, search, social networking and e-commerce.

Total data center infrastructure equipment revenues, including both cloud and non-cloud, hardware and software, were $38 billion in Q3. Servers, OS, storage, networking and virtualization software combined accounted for 96% of the data center infrastructure market, with the balance comprised of network security and management software. Dell EMC is the leader in both server and storage revenues, while Cisco is dominant in the networking segment. Microsoft and VMware feature heavily in the vendor rankings due to their leadership positions in server OS and virtualization applications respectively. Outside of these four, the other leading vendors in the market are HPE, Huawei, Inspur, and Lenovo. ODMs in aggregate also feature heavily in the vendor rankings, thanks to their activities supplying hardware to hyperscale operators. Inspur and Huawei are the major vendors that achieved the strongest growth in 2019.

“We are seeing very different scenarios play out in terms of data center spending by hyperscale operators and enterprises,” said John Dinsdale, a Chief Analyst at Synergy Research Group. “On the one hand revenues at the hyperscale operators continue to grow strongly, driving increased demand for data centers and data center hardware. There is an ever-increasing number of hyperscale data centers, many of which continue to be expanded. Those huge data centers are crammed full of servers and other hardware which are on a frequent refresh cycle. On the other hand we see a continued decline in the volume of servers being bought by enterprises. The impact of those declines is balanced by steady increases in server average selling prices, as IT operations demand ever-more sophisticated server configurations, but overall spending by enterprises remains almost flat. These trends will continue into the future.”

About Synergy Research Group

Synergy Research Group delivers quarterly analyses of global IT and Cloud markets, offering detailed breakouts of vendor revenues and shipments by segment and region. Market shares and forecasts are provided through Synergy Interactive Analysis (SIA™) — the industry's only fully proprietary SaaS platform purpose-built for market share and forecasting analytics.

For more than 25 years, Synergy has been a trusted source of quantitative research and market intelligence across emerging communications and technology sectors. By combining syndicated research with specialized consulting, we deliver actionable intelligence to marketing and strategy executives worldwide.

Subscriptions: sales@srgresearch.com

Press inquiries: hgallo@srgresearch.com

A trusted source of accurate market data, Synergy is cited by industry leaders as well as leading financial, business, and trade publications such as The Economist, The New York Times, The Wall Street Journal, United States Federal Reserve Board, NPR, Forbes, Bloomberg, Financial Times, Bank of England, Fortune, and The Guardian.