Half-Year Capex Analysis – Telcos Flat; Enterprise Nudges Up; Hyperscale Boom Continues

RENO, NV, September 1, 2021

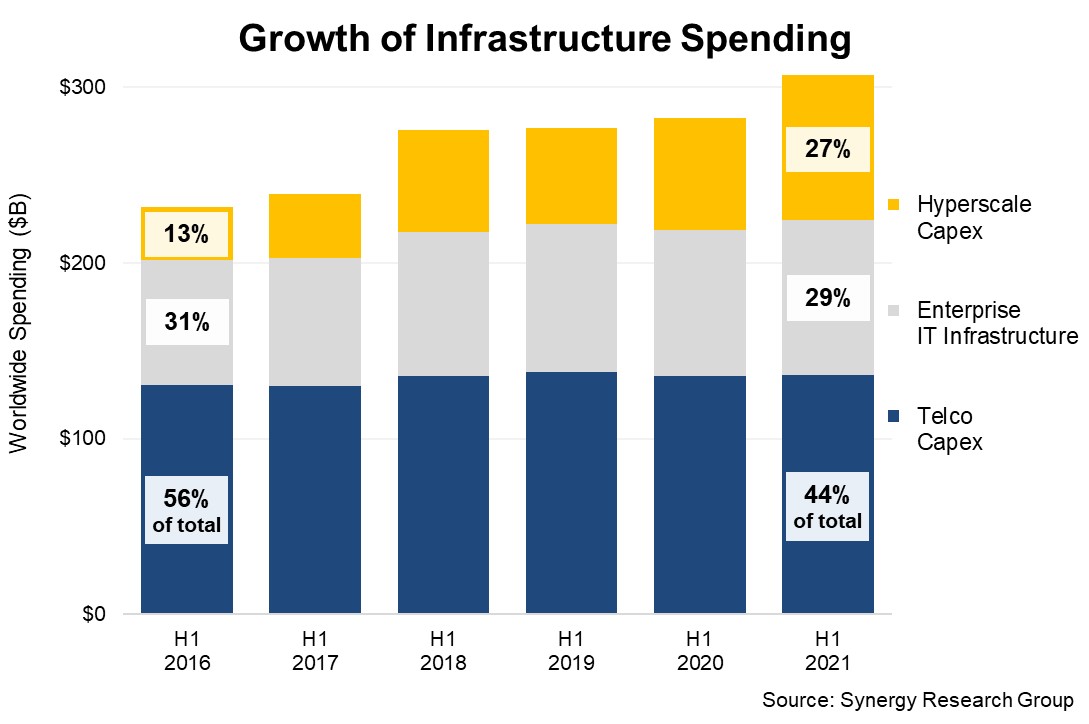

New data from Synergy Research Group shows that telco capex levels in the first half were once again flat while hyperscale operator capex shot up by another 30%. Meanwhile enterprise spending on IT infrastructure recovered a little and grew by 6%. These numbers largely reflect the longer term trends which show that telco capex has essentially been static for the last six years while hyperscale operator spending has almost tripled and enterprise IT infrastructure spending has grown by 23%. Across the three groups infrastructure spending in the first half passed the $300 billion mark with hyperscale operators now accounting for 27% of the total, up from just 13% in the first half of 2016. Over that six-year period, enterprise share of the total has hovered around the 30% mark while telco share has fallen from 56% to 44%. Total spending in the first half of 2021 was $307 billion, having grown by 9% from 2020 and by an average of 6% per year since 2016. The data covers total capital expenditure for telcos and hyperscale operators, which is mostly focused on networking and data center hardware and software. To make the numbers more comparable, for enterprises it covers spending on IT infrastructure, which is primarily data centers, networking and collaboration tools. It excludes enterprise spending on communication and IT services, devices and business software. Hyperscale operators include the 19 companies that meet Synergy’s criteria for being considered hyperscale, with the biggest spenders in the first half being Amazon, Microsoft, Google, Facebook, Apple, Alibaba and ByteDance. Telcos include both fixed and mobile operations, with the biggest spenders in the first half being China Mobile, Deutsche Telekom, NTT, Verizon, AT&T, Vodafone and Orange.

Total spending in the first half of 2021 was $307 billion, having grown by 9% from 2020 and by an average of 6% per year since 2016. The data covers total capital expenditure for telcos and hyperscale operators, which is mostly focused on networking and data center hardware and software. To make the numbers more comparable, for enterprises it covers spending on IT infrastructure, which is primarily data centers, networking and collaboration tools. It excludes enterprise spending on communication and IT services, devices and business software. Hyperscale operators include the 19 companies that meet Synergy’s criteria for being considered hyperscale, with the biggest spenders in the first half being Amazon, Microsoft, Google, Facebook, Apple, Alibaba and ByteDance. Telcos include both fixed and mobile operations, with the biggest spenders in the first half being China Mobile, Deutsche Telekom, NTT, Verizon, AT&T, Vodafone and Orange.

“There is an increasingly sharp contrast in spending patterns across the three main industry sectors,” said John Dinsdale, a Chief Analyst at Synergy Research Group. “Telcos remain locked in a low-to-no growth world and their capex reflects that. While there were big hopes for 5G, it has proven to be a case of changing the mix of investments within relatively fixed budgets, rather than substantially growing overall telco spend. That picture is unlikely to change too much over the next few years. Meanwhile hyperscale operator revenues are currently growing by over 30% per year, which has required them to grow their spending at a somewhat similar rate. Those growth rates will moderate a bit over the coming years but will be viewed jealously by the telco world. The enterprise picture is more complex with cloud, big data and increasingly sophisticated collaboration requirements driving a multitude of changes in their IT operations, but on balance we should continue to see modest growth in their infrastructure spending.”

About Synergy Research Group

Synergy Research Group, now part of TechInsights, delivers quarterly analyses of global IT and Cloud markets, offering detailed breakouts of vendor revenues and shipments by segment and region. Market shares and forecasts are provided through Synergy Interactive Analysis (SIA™) — the industry's only fully proprietary SaaS platform purpose-built for market share and forecasting analytics.

For more than 25 years, Synergy has been a trusted source of quantitative research and market intelligence across emerging communications and technology sectors. By combining syndicated research with specialized consulting, we deliver actionable intelligence to marketing and strategy executives worldwide.

A trusted source of accurate market data, Synergy is cited by industry leaders as well as leading financial, business, and trade publications such as The Economist, The New York Times, The Wall Street Journal, United States Federal Reserve Board, NPR, Forbes, Bloomberg, Financial Times, Bank of England, Fortune, and The Guardian.

About TechInsights

Regarded as the most trusted source of actionable, in-depth intelligence related to semiconductor innovation and surrounding markets, TechInsights’ content informs decision makers and professionals whose success depends on accurate knowledge of the semiconductor industry—past, present, or future.

Over 650 companies and 100,000 users access the TechInsights Platform, the world’s largest vertically integrated collection of unmatched reverse engineering, teardown, and market analysis in the semiconductor industry. This collection includes detailed circuit analysis, imagery, semiconductor process flows, device teardowns, illustrations, costing and pricing information, forecasts, market analysis, and expert commentary. TechInsights’ customers include the most successful technology companies who rely on TechInsights’ analysis to make informed business, design, and product decisions faster and with greater confidence. For more information, visit www.techinsights.com.

Subscriptions: sales@srgresearch.com

Press inquiries: heather.gallo@techinsights.com