GenAI Helps Drive Quarterly Cloud Revenues to $119 Billion as Growth Rate Jumped Yet Again in Q4

RENO, NV, February 5, 2026

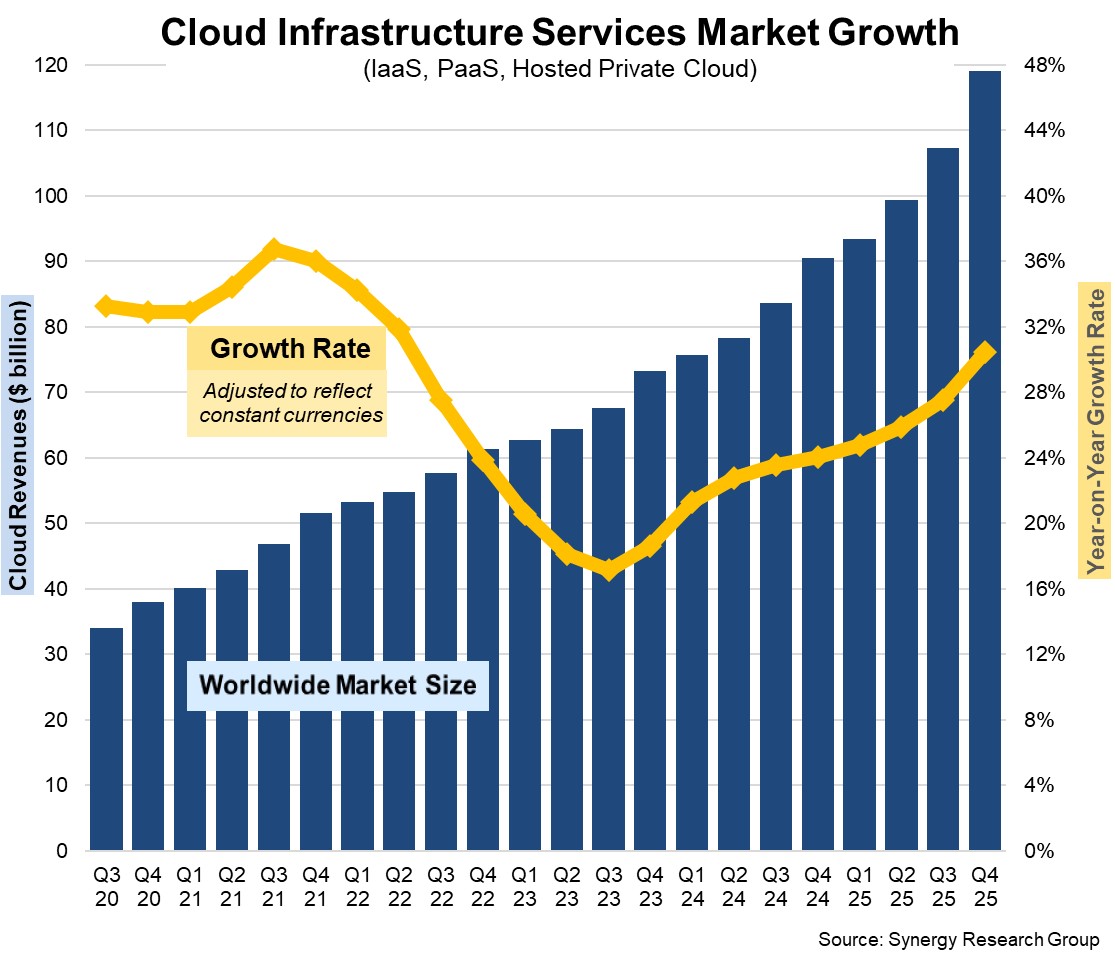

New data from Synergy Research Group shows that Q4 enterprise spending on cloud infrastructure services jumped by almost $12 billion from the previous quarter and by $29 billion from Q4 of 2024. The scale of these increments far surpasses anything previously seen in this market. The 2025 full-year market reached $419 billion. Backing out the impact of some major currency fluctuations over the period, this represents growth of 30% from the fourth quarter of last year. This marks the ninth consecutive quarter of accelerating year-on-year growth and the highest growth rate the market has seen in more than three years. GenAI is clearly the primary driver of these changing market dynamics. Among the major cloud providers, Amazon maintains a strong lead in the market, though Microsoft and Google continue to achieve substantially higher growth rates. Their Q4 worldwide market shares were 28%, 21%, and 14% respectively. Among the tier two cloud providers, those with the highest growth rates include CoreWeave, OpenAI, Oracle, Crusoe, and Nebius. From a virtual standing start just two years ago, CoreWeave is now generating more than $1.5 billion in quarterly cloud revenue and has joined the top ten cloud providers, driven by its AI- and GPU-focused services. With most of the major cloud providers having now released their earnings data for Q4, Synergy estimates that quarterly cloud infrastructure service revenues (including IaaS, PaaS and hosted private cloud services) were $119.1 billion, with full-year 2025 revenues reaching $419 billion. Public IaaS and PaaS services account for the bulk of the market, and those grew by 34% in Q4. The dominance of the major cloud providers is even more pronounced in public cloud, where the top three account for 68% of the market. Geographically, the cloud market continues to grow strongly in all regions of the world. When measured in local currencies, the major countries with the strongest growth included Australia, India, Indonesia, Ireland, Mexico, South Africa, and Taiwan, all growing at rates above the worldwide average. The US remains by far the largest cloud market, with its scale far surpassing the whole APAC region. The US market grew by 30% in Q4. In Europe the largest cloud markets are the UK and Germany, but the big markets with the highest growth rates were Ireland, Poland and Sweden.

With most of the major cloud providers having now released their earnings data for Q4, Synergy estimates that quarterly cloud infrastructure service revenues (including IaaS, PaaS and hosted private cloud services) were $119.1 billion, with full-year 2025 revenues reaching $419 billion. Public IaaS and PaaS services account for the bulk of the market, and those grew by 34% in Q4. The dominance of the major cloud providers is even more pronounced in public cloud, where the top three account for 68% of the market. Geographically, the cloud market continues to grow strongly in all regions of the world. When measured in local currencies, the major countries with the strongest growth included Australia, India, Indonesia, Ireland, Mexico, South Africa, and Taiwan, all growing at rates above the worldwide average. The US remains by far the largest cloud market, with its scale far surpassing the whole APAC region. The US market grew by 30% in Q4. In Europe the largest cloud markets are the UK and Germany, but the big markets with the highest growth rates were Ireland, Poland and Sweden.

“We said that Q3 market numbers were very impressive, but they pale by comparison with Q4. Growth rates like these have not been seen since early 2022, when the market was less than half the size it is today,” said John Dinsdale, Chief Analyst at Synergy Research Group. “GenAI has simply put the cloud market into overdrive. AI-specific services account for much of the growth since 2022, but AI technology has also enhanced the broader portfolio of cloud services, driving revenue growth across the board. The leading cloud providers have all seen their revenue growth rates jump. Meanwhile, neoclouds remain relatively small compared with the leaders, but they too are now contributing meaningful incremental growth.”

About Synergy Research Group

Synergy Research Group, now part of TechInsights, delivers quarterly analyses of global IT and Cloud markets, offering detailed breakouts of vendor revenues and shipments by segment and region. Market shares and forecasts are provided through Synergy Interactive Analysis (SIA™) — the industry's only fully proprietary SaaS platform purpose-built for market share and forecasting analytics.

For more than 25 years, Synergy has been a trusted source of quantitative research and market intelligence across emerging communications and technology sectors. By combining syndicated research with specialized consulting, we deliver actionable intelligence to marketing and strategy executives worldwide.

A trusted source of accurate market data, Synergy is cited by industry leaders as well as leading financial, business, and trade publications such as The Economist, The New York Times, The Wall Street Journal, United States Federal Reserve Board, NPR, Forbes, Bloomberg, Financial Times, Bank of England, Fortune, and The Guardian.

About TechInsights

Regarded as the most trusted source of actionable, in-depth intelligence related to semiconductor innovation and surrounding markets, TechInsights’ content informs decision makers and professionals whose success depends on accurate knowledge of the semiconductor industry—past, present, or future.

Over 650 companies and 100,000 users access the TechInsights Platform, the world’s largest vertically integrated collection of unmatched reverse engineering, teardown, and market analysis in the semiconductor industry. This collection includes detailed circuit analysis, imagery, semiconductor process flows, device teardowns, illustrations, costing and pricing information, forecasts, market analysis, and expert commentary. TechInsights’ customers include the most successful technology companies who rely on TechInsights’ analysis to make informed business, design, and product decisions faster and with greater confidence. For more information, visit www.techinsights.com.

Subscriptions: sales@srgresearch.com

Press inquiries: heather.gallo@techinsights.com