Emerging Opportunities and Perils of All Things Cloud: Will vendors and service providers co-exist in blissful matrimony or is chance of divorce high?

Reno, NV - Cloud is one of the most exciting things to happen in IT and computing today. It is the promise to provide a world of computational utility and innovative commercial and consumer services. From using Force.com, WebEx, Amazon’s AWS, Microsoft Azure, Google Apps, Netflix, or a growing list of SaaS services, Cloud technology is happening and happening fast. And unlike any other IT or advanced communication innovations in the past, Cloud is not just an occurrence on one or two continents but is truly finding fast acceptance in developed and emerging economies around the world.

Therefore it is with a deep, geekish heart-felt love of technology that I believe Cloud is the quintessential marriage of computing and communications—providing some really cool new things, as well as shaking up the landscape of who is a competitor, who is a partner, and who could be the next big threat in the community of vendors and service providers. It is this curious dynamic that spells opportunity or fear depending on who you are today and what you plan to be tomorrow.

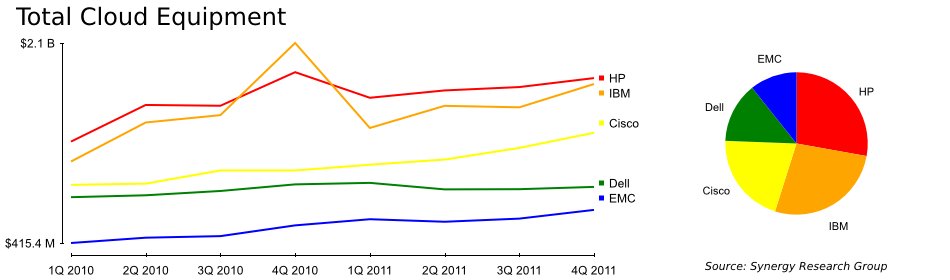

Here at Synergy we spend our days counting things and identifying emerging trends in the world of computing and communications. To the howl and cry of many that say Cloud is an over-hyped concept fueled by mega-marketing budgets, I have to point to the size of this market. In 2011, the sales of Cloud Equipment grew to $39 Billion, an increase of 15% over 2010 and the growth is beginning to accelerate. The top five vendors that are reaping the large investments in Cloud are HP, IBM, Cisco, Dell, and EMC (in ranked order).

Synergy defines cloud equipment as virtualized data centers and/or data centers that provide self-provisioning services such as SaaS, IaaS, or PaaS. In non-geek speak, it is the gear that makes it possible to watch movies on NetFlix, do cool things with your smart phone, do a book report using Google Apps, or crunch your personal finances on Quickbooks.

And to us IT geeks this is just the tip of the iceberg. Ultimately Cloud technology represents the potential of outsourcing data centers—both big and small. The ability to turn a costly capital investment and maintenance into a monthly subscription cost, in addition to radically reducing overall IT expense, has the capability to minimize the cost of the $10B spent per year on Enterprise software applications. The point here is there is a decent amount of momentum driving Cloud—from commercial to consumer applications—on many different angles all along the spectrum. And now that the proverbial genie is out of the bottle, Cloud is here to stay.

So all this robust opportunity hints at a very large market for vendors and service providers in which to sell. And for the service providers it could be a watershed to move away from the broken business models many are straddled with to an opportunity to re-tool and re-calibrate their models.

The thing is, Synergy has followed this market for over two decades and a question keeps gnawing at me: Are the vendors and service providers headed on a collision course where they become head-to-head competitors? Or, will a collaborative world arise after the dust settles; a world where the two groups can leverage each of their unique strengths and exist as partners?

Honestly, I think it’s both a simple and complex question with a simple and complex answer. The simple, and more plausible answer is that vendors who choose to offer SaaS services (such as NEC, Cisco, or Microsoft) can find common ground and co-exist with service providers. As an example, we can point to Cisco’s partnering with AT&T, Orange, Sprint and Verizon enabling those service providers to offer SaaS Collaboration services. The more complicated and unappealing answer is that if a vendor decides to go it alone and build-out its own IaaS and PaaS service offering it could spell trouble and potentially ruin a could-be-good-relationship with service providers.

Case in point: HP, the number one provider of Cloud Equipment has chosen to offer their own HP branded Public Cloud offering. Sounds great for HP. But that will put HP in a direct confrontational role to existing IaaS and PaaS providers from AT&T to Amazon; the very same companies to which HP would want to sell lots of servers or networking equipment. It’s quandaries such as this that causes me pause: HP is a big company so there must be a big strategy; therefore, I must be missing something. Alas, I am left scratching my head on this one given that HP’s blade server business is under increasing competitive pressure from Cisco and IBM. More poignantly, Cisco is now the number three player in Blade Servers. This move by HP could make a bad situation worse.

If we look to see how IBM and Cisco (as well as EMC, NetApp, and VMware) are approaching the public Cloud opportunity, there appears to be a consistent understanding that in the world of Cloud, no one can go it alone and partnering with each other and working closely with service providers is the path where everyone eventually ends up.

Ultimately the stakes are really high for both vendors and service providers. Let me lay it out from the work we have done here at Synergy. For vendors it’s about selling more equipment; that is the servers, storage, networking gear and associated software that go into a “Cloud” data center. Synergy forecasts this market to approach a market size nearing $100B over the next four years. Both Private networks (i.e. Enterprises) and service providers, such as the AT&Ts, SingTels, and British Telecoms of the world, buy this equipment. The service provider portion of this CapEx spending looks to increase.

In turn, the service providers deploy this equipment to their data center build-outs so that they can sell and market their very own public Cloud services. Today that revenue opportunity is well under 10% of a SP’s enterprise service revenues, but the room for growth is quite compelling, and we believe it will increase aggressively over the next five years.

As it stands, services providers are hunting for a way to better capitalize on the services where they excel and defining what assets they can further monetize. Cloud is a refreshing bright spot on the horizon in which SPs are actively looking. We are seeing more and more interesting partnerships with vendors and service providers where vendors are actively working with SPs to assist in the build-out and operation of these new services. Some collaborative partnering thus far that looks to be promising include SingTel partnering with Huawei and Orange partnering with Cisco.

Synergy predicts that those vendors that can move past the initial proposal and subsequent engagement and can actually assist and work together in building-out Public Cloud networks while maintaining a collaborative working relationship with service providers will fair far better than a vendor who decides to go it alone. As long as that relationship can last beyond the honeymoon phase and prepare to settle in for the long—but rewarding—haul that is a successful marriage.

About Synergy Research Group

Synergy Research Group delivers quarterly analyses of global IT and Cloud markets, offering detailed breakouts of vendor revenues and shipments by segment and region. Market shares and forecasts are provided through Synergy Interactive Analysis (SIA™) — the industry's only fully proprietary SaaS platform purpose-built for market share and forecasting analytics.

For more than 25 years, Synergy has been a trusted source of quantitative research and market intelligence across emerging communications and technology sectors. By combining syndicated research with specialized consulting, we deliver actionable intelligence to marketing and strategy executives worldwide.

Subscriptions: sales@srgresearch.com

Press inquiries: hgallo@srgresearch.com

A trusted source of accurate market data, Synergy is cited by industry leaders as well as leading financial, business, and trade publications such as The Economist, The New York Times, The Wall Street Journal, United States Federal Reserve Board, NPR, Forbes, Bloomberg, Financial Times, Bank of England, Fortune, and The Guardian.