Cloud: Competition or Collaboration?

With all the changes that cloud creates, Synergy believes some key players will be tempted to compete against their own customers while others will seek a more collaborative outcome.

Cloud is one of the most exciting things to happen in IT and computing today. The promise of profound changes in the immediate future is something we all should be thrilled about. From the entertainment and communication sectors in which we engage as consumers, to the business applications that enable us to become increasingly productive, competitive, and successful, cloud is a true watershed with profound and far-reaching implications as significant as the invention of the TCP/IP protocol, mainframes, PCs, or the first web browser.

The concepts behind cloud have been discussed since the 1950s (take a look at the views of people like Herb Grosch, John McCarthy and Douglas Parkhill), though it wasn’t until recently that three factors have come together to turn the cloud vision into reality: computer commoditization, virtualization, and the expansion of the high speed Internet. These three trends in concert with each other have created what is likely the next chapter in the narrative that is the computing and communications story. And this story is being written blisteringly fast. From using Force.com, WebEx, Amazon’s AWS, Microsoft Azure, Google Apps, Netflix or a growing list of SaaS services, cloud technology is happening.

In 2011, the sales of cloud equipment grew to $39 Billion, an increase of 15% over 2010, and the growth is beginning to accelerate. Synergy defines cloud equipment as virtualized data centers and/or data centers that provide self-provisioning services such as SaaS, IaaS, or PaaS. That is the gear and technology that makes it possible to watch movies on NetFlix, use smartphones in innovative ways, play games, or crunch personal finances on Quickbooks; simply put, it’s the delivery of digital content and services.

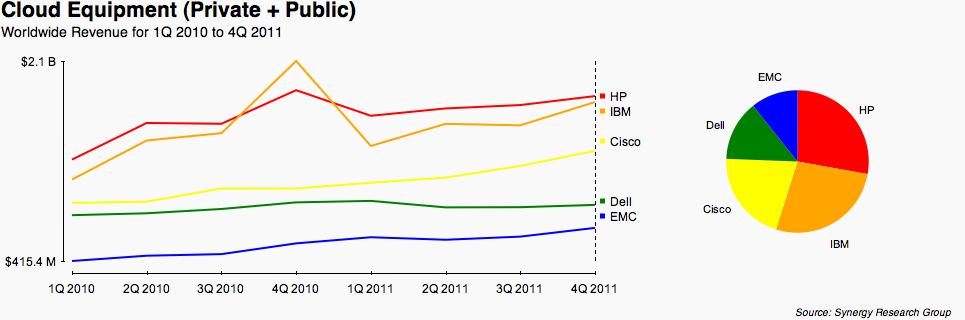

The top five vendors that are reaping the large investments in cloud are HP, IBM, Cisco, Dell, and EMC (in ranked order). What’s interesting and important to point out is that traditional telecom service providers are now purchasing a significant amount of cloud equipment.

In turn, these service providers deploy this equipment to their data center build-outs so that they can sell and market their very own public cloud services. Today that revenue opportunity does not come close to their overall revenues, but the room for growth is quite compelling and Synergy believes it will increase substantially over the next five years.

As it stands, services providers are hunting for a way to capitalize on the services where they already excel, and, at the same time define what assets they can further monetize. Cloud is such an asset. We are seeing more and more interesting partnerships between vendors and service providers where vendors are actively working with SPs to assist in the build-out and operation of these new services.

However, with the cloud services market expected to approach $100 billion per year, many competing interests are beginning to pop up. And given that cloud removes substantial barriers of entry that allow vendors and providers to go after the same customers, it creates a new world where one can expect to see an interesting churn of creative collaboration and the temptation for some to directly compete against their customers.

Over the last decade, we have seen traditional service providers forced to redefine their consumer and commercial services in the face of new technologies and competitors. The service providers take a lot of criticism that they are too big or too slow, or even, that they are not doing a good enough job keeping up with the varying trends in technology. However, when we look at the revenues of the top 100 service providers, their service revenues remain significant and, more importantly, are showing growth. A recent study from our research partner, Telegeography, shows the world’s top 100 telecoms service providers grew their revenues 5.6% from 2010 to 2011 to reach $1.7 trillion. Significantly, of this $1.7 trillion revenue, 15% is being generated from non-telecom services.

One of the fast areas of revenue growth for service providers has been with managed services. Major countries around the globe have seen service providers expanding their managed service offerings. And with all the glowing opportunities that cloud enables, service providers are in a very good position to provision existing managed services over a cloud architecture reaping the economic benefits of increasing revenues and reducing operational expenses. This same economic benefit will also play out with their consumer businesses such as video, pay-TV, mobile data, and a host of emerging broadband services.

Considering the capital that has been invested by service providers in data center build-outs within the last decade, Synergy believes they have a significant opportunity to capitalize on their existing infrastructure investments and go beyond managed services to provide advanced cloud services. Interestingly enough, some service providers are beginning to acquire data centers outside of their traditional geographic markets, either an attempt to play catch-up or to become a competitive force outside of their traditional markets. As an example, NTT just acquired an 85% stake in Gyron, a UK data center, with the goal to extend its cloud services capabilities to multi-site global companies.

Service providers certainly have the capital to be a very big player in cloud and are clearly showing signs that they are on the move. It makes good sense that it would be better to look for ways of partnering with service providers rather than competing against them.

Service providers clearly need assistance in some key strategic areas. Synergy believes this weakness is an exploitable opportunity for vendors and, perhaps, a chance to forge some strong relationships. For example, when it comes to building and provisioning collaboration hosted and cloud services, this falls more into the expertise of the traditional enterprise UC players such as Cisco, Avaya, Microsoft, Mitel, and Shoretel.

In the US, we have seen Cisco build and foster strong relationships with AT&T and Verizon. And in EMEA, we have seen the same level of partnering with Orange. Cisco is very clear that it is partnering with service providers and other channel partners in marketing its SaaS conferencing services. Service providers could develop their own WebEx-like services but in our opinion it would be a better outcome for them to partner with vendors who have the expertise versus building a feature rich UC service from scratch. Partnering, rather than inappropriate competition, is key to success in the market.

There are some who appear to be setting themselves up to compete against their own partners or customers. Two top-of-mind examples are HP and Amazon/Heroku.

From a public cloud perspective, we can see the allure that a server company would want to expand its business to sell servers as well as provide their own public cloud IaaS offering. A case in point - HP, the number one provider of cloud equipment, has recently launched its own HP-branded public cloud offering.

This could prove to be a good opportunity for HP but by launching its own public cloud service, it is now in direct competition with its customers who offer public cloud services.

And this certainly does not come at a good time for HP as its executive leadership has been in flux and its core businesses are under increased competitive pressure. However, given that HP has a very loyal customer base it may have some success with its foray into public cloud services. Synergy believes that this behavior poses a serious risk of ostracizing future server sales to traditional service provider customers (e.g. AT&T, Verizon, BT, etc.) and emerging service providers (e.g. Amazon, Rackspace, etc.). HP’s desire to move into public cloud services represents a major shift and will only happen if HP’s executive management sees this as a serious strategic area of focus that it cannot afford to miss. Given its recent flopping strategy in its core businesses, breaking apart servers and the printer businesses and now bringing them back together again, this is reason for concern as to how committed HP will be in the public cloud game.

A different type of example of the possible stresses caused by cloud growth opportunity is provided by Amazon. Amazon is the gold standard for IaaS public cloud services; it still maintains its first-to-market advantage and remains in a position where it can truly determine its destiny. Amazon’s behavior indicates that it wants to dominate as much as it can in the consumer cloud, be it the Kindle or its own web browser to the massive storefront that looms over its cloud infrastructure. In addition to the consumer cloud, it maintains its dominance in public cloud with its IaaS service, AWS.

Of all the disruption that cloud makes possible, PaaS vendors and services look to be the most vulnerable. One of Amazon’s partners, Heroku, is the leading provider of PaaS cloud services - and it is in danger of being left at the alter. Heroku’s PaaS service, which it sells to its own customers, partners with Amazon to provision its services over Amazon’s AWS IaaS infrastructure. Take a look at Amazon’s growing list of AWS services and there appears a growing list of PaaS type services. Additionally, Amazon is absorbing some aspects of PaaS services into its existing AWS services. If Amazon wakes up one day and decides to absorb all of PaaS, it could potentially be a bad break-up for Heroku.

To highlight the fluidness of all things cloud, Salesforce.com purchased Heroku in 2010, so that Salesforce.com could also expand from their SaaS offerings to also provide PaaS services.

Summary

Look forward into the future and think of the interactions of a worldwide community of wireline broadband subscribers, smartphones and other mobile devices accessing the cloud, and the opportunities begin to exponentially expand. Then throw in the astronomical amount of devices that IPv6 now makes possible to connect to the Internet and suddenly the capability of everyone and everything communicating with each other all the time over the cloud is possible—be it people to people, machines to machines, or people to machines.

The stakes are high, and the service providers are serious about moving into this market. Some vendors will choose to find opportunity in this trend by partnering and at the other end of the spectrum some vendors will choose to compete against the service providers.

For the later group, Synergy thinks that vendors will get further ahead by working with the biggest spenders for cloud equipment (the service providers), rather than setting up a situation in which their main opponent is themselves.

About Synergy Research Group

Synergy Research Group delivers quarterly analyses of global IT and Cloud markets, offering detailed breakouts of vendor revenues and shipments by segment and region. Market shares and forecasts are provided through Synergy Interactive Analysis (SIA™) — the industry's only fully proprietary SaaS platform purpose-built for market share and forecasting analytics.

For more than 25 years, Synergy has been a trusted source of quantitative research and market intelligence across emerging communications and technology sectors. By combining syndicated research with specialized consulting, we deliver actionable intelligence to marketing and strategy executives worldwide.

Subscriptions: sales@srgresearch.com

Press inquiries: hgallo@srgresearch.com

A trusted source of accurate market data, Synergy is cited by industry leaders as well as leading financial, business, and trade publications such as The Economist, The New York Times, The Wall Street Journal, United States Federal Reserve Board, NPR, Forbes, Bloomberg, Financial Times, Bank of England, Fortune, and The Guardian.