2022 Capex Analysis – Growth in Hyperscale and Enterprise Spending; Telco Remains in the Doldrums

RENO, NV, January 26, 2023

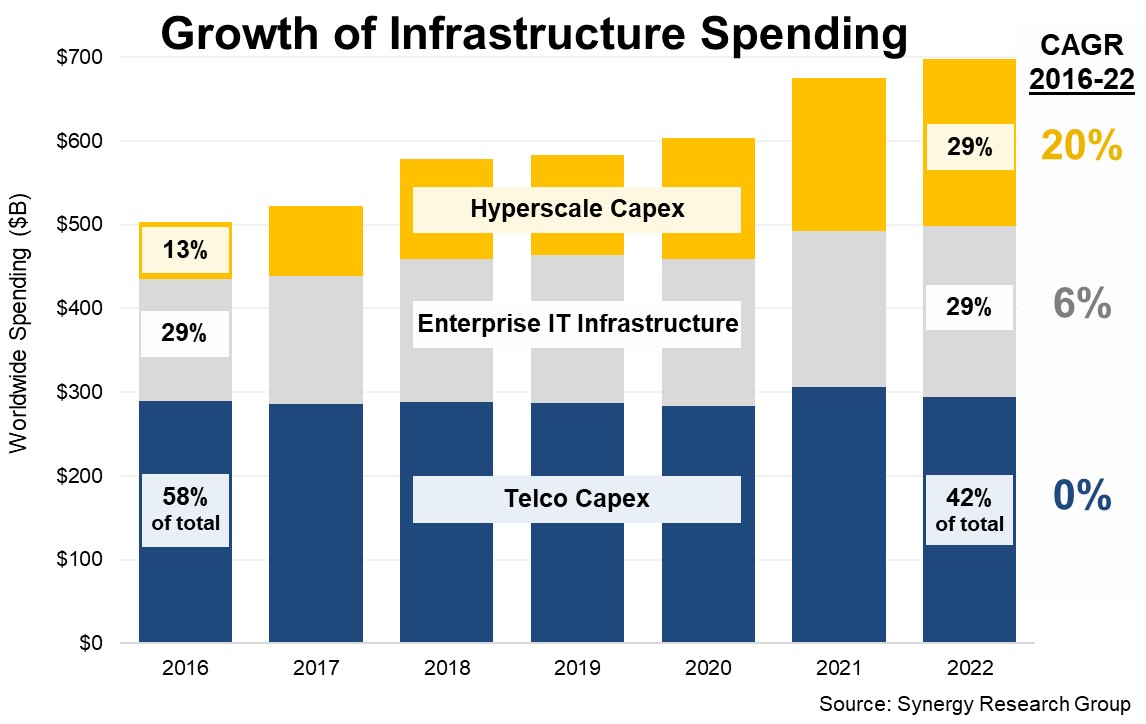

New data from Synergy Research Group shows that both hyperscale operator capex and enterprise spending on IT infrastructure grew by 9% in 2022, while telco capex dropped by 4%. Across the three groups, infrastructure spending in 2022 reached $700 billion, with hyperscale operators now accounting for 29% of the total, up from just 13% in 2016. Over that period, enterprise share of the total has hovered around the 29% mark while telco share has fallen from 58% to 42%. Since 2016 hyperscale capex has grown by an average of 20% per year, while enterprise IT spending has grown by an average 6% and telco capex has been flat. In aggregate, spending has increased by an average 6% per year since 2016. The data covers total capital expenditure for telcos and hyperscale operators, which is mostly focused on networking and data center hardware and software. To make the numbers more comparable, for enterprises the data covers spending on IT infrastructure, which is primarily data centers, networking and collaboration tools. It excludes enterprise spending on communication and IT services, devices and business software. Hyperscale operators include the 19 companies that meet Synergy’s criteria for being considered hyperscale, with the biggest spenders being Amazon, Google, Facebook, Microsoft, Apple, Alibaba and ByteDance. Telcos include both fixed and mobile operations, with the biggest spenders being China Mobile, Deutsche Telekom, Verizon, AT&T, NTT and China Telecom. The 2022 numbers are based on actual data for the first three quarters of the year plus Synergy forecasts for the fourth quarter.

The data covers total capital expenditure for telcos and hyperscale operators, which is mostly focused on networking and data center hardware and software. To make the numbers more comparable, for enterprises the data covers spending on IT infrastructure, which is primarily data centers, networking and collaboration tools. It excludes enterprise spending on communication and IT services, devices and business software. Hyperscale operators include the 19 companies that meet Synergy’s criteria for being considered hyperscale, with the biggest spenders being Amazon, Google, Facebook, Microsoft, Apple, Alibaba and ByteDance. Telcos include both fixed and mobile operations, with the biggest spenders being China Mobile, Deutsche Telekom, Verizon, AT&T, NTT and China Telecom. The 2022 numbers are based on actual data for the first three quarters of the year plus Synergy forecasts for the fourth quarter.

Hyperscale operator share of total spending has continued to rise steadily over the last few years, as continued growth in cloud and other digital services drive ever-higher spending levels. Telco spending remains heavily crimped by lack of meaningful growth in their revenue streams. Enterprise spending has also bounced back in the last two years after a soft spell in 2019 and 2020. The main drivers in the enterprise have been the continued long-term growth of hosted and cloud collaboration solutions, increased spending on network security, and a post-pandemic bounce back for both enterprise data centers and switches. In some segments, higher ASPs have also contributed, as cost increases due to supply chain issues are passed on to the customers of tech vendors.

About Synergy Research Group

Synergy Research Group delivers quarterly analyses of global IT and Cloud markets, offering detailed breakouts of vendor revenues and shipments by segment and region. Market shares and forecasts are provided through Synergy Interactive Analysis (SIA™) — the industry's only fully proprietary SaaS platform purpose-built for market share and forecasting analytics.

For more than 25 years, Synergy has been a trusted source of quantitative research and market intelligence across emerging communications and technology sectors. By combining syndicated research with specialized consulting, we deliver actionable intelligence to marketing and strategy executives worldwide.

Subscriptions: sales@srgresearch.com

Press inquiries: hgallo@srgresearch.com

A trusted source of accurate market data, Synergy is cited by industry leaders as well as leading financial, business, and trade publications such as The Economist, The New York Times, The Wall Street Journal, United States Federal Reserve Board, NPR, Forbes, Bloomberg, Financial Times, Bank of England, Fortune, and The Guardian.